On July 4, 2025, while Americans were firing up grills and watching fireworks, something else major happened: the OneBig Beautiful Bill Act (OBBBA) was signed into law. And with it came comprehensive updates to the tax code.

If you’re a property owner, investor, business owner, or just someone trying to stay ahead of tax changes, this law brings a mix of opportunities and trade-offs. Some temporary benefits have now become permanent. Others are heading out the door.

This article covers changes to itemized deductions, estate planning, business expenses and more. Whether you’re filing as an individual or managing a pass-through entity, we help you understand how the OBBBA may impact you.

Provisions extended from the 2017 Tax Cuts and Jobs Act

The centre of OBBBA is the permanent extension of many key tax breaks that people speculated may expire at the end of 2025. Those familiar with the 2017 Tax Cuts and Jobs Act (TCJA) may recognize some of these provisions.

● Lower Tax Rates Stay in Place

The top federal income tax rate remains at 37%, rather than reverting to the 39.6% scheduled increase. This continuation particularly benefits high earners.

● Standard Deduction Remains Higher

Under OBBB, the higher standard deduction first introduced in 2017 is now permanent, with 2025 amounts set at $15,750 for single filers and $31,500 for married couples filing jointly. A relief for those who were concerned they’d drop back to pre-2017 levels.

Plus, taxpayers age 65 and older now get an additional $6,000 deduction each, or $12,000 total for married couples in that age group.

● Mortgage Interest and PMI Deductions

The cap on mortgage interest remains at $750,000 of acquisition debt. What’s new is the renewed ability to deduct mortgage insurance premiums, a boost for those who bought homes with smaller down payments.

● 2% Miscellaneous Deduction Still Off the Table

OBBBA further suspends the 2% miscellaneous itemized deduction. That includes expenses like investment advisor fees, tax prep fees and unreimbursed employee expenses. However, qualified educators can now deduct more of their out-of-pocket classroom-related costs.

● Child Tax Credit Improved

The Child Tax Credit gets further enhancements, though the specifics depend on income and filing status. Generally, it’s been expanded in a way that makes it more accessible to a broader range of taxpayers.

● Qualified Business Income Deduction Made Permanent

The popular §199A 20% deduction for pass-through businesses is now permanent. This helps sole proprietors, partnerships and S corporations continue to deduct a portion of their qualified income.

● Estate and Gift Tax Exemption Increased

Starting January 1, 2026, the unified estate and gift tax exemption increases to $15 million. That’s a significant planning opportunity for high-net-worth families looking to transfer wealth tax-efficiently.

SALT deduction raised, but only temporarily

For itemizers, the state and local tax (SALT) deduction cap has been an ongoing frustration for some tax filers. OBBBA raises the cap from $10,000 to $40,000, but only for five years. And there’s something else to note.

The increased deduction phases out for higher earners. If your income exceeds certain thresholds, you may not see the full benefit of the higher cap. So while this may look like a win on paper, strategic planning is still essential to get the most out of it.

Pass-Through Entity (PTE) tax elections remain untouched

Good news for owners of pass-through entities: while earlier versions of OBBBA floated restrictions on PTE tax elections, the final version leaves them unchanged.

If you’re using the PTE election to bypass the SALT cap and deduct state taxes at the entity level, you can keep doing so.

This is especially beneficial in high-tax states where individual SALT deductions are still capped. With the higher federal SALT limit being both temporary and reduced for high earners, the PTE election remains a savvy tax strategy to consider.

New limits on itemized deductions and return of the AMT

● Itemized Deduction Limits Are Back

OBBBA introduces new limits on certain itemized deductions. These apply once you pass specific income thresholds and may reduce the total value of your itemized write-offs.

● Alternative Minimum Tax (AMT) Reinstated

After a period of limited application, the Alternative Minimum Tax is back. The AMT was designed to ensure that high earners pay a minimum amount of tax, even after deductions.

If your income is high and your return relies heavily on deductions, it may be time to revisit your tax strategy.

Disaster relief for 2025 events

If you’re affected by a federally declared disaster in 2025, OBBBA includes provisions that could ease your tax burden. This may consist of faster loss write-offs, expanded casualty loss deductions, or access to penalty-free retirement withdrawals.

As always, you’ll need documentation. But if disaster strikes, relief may be available to you.

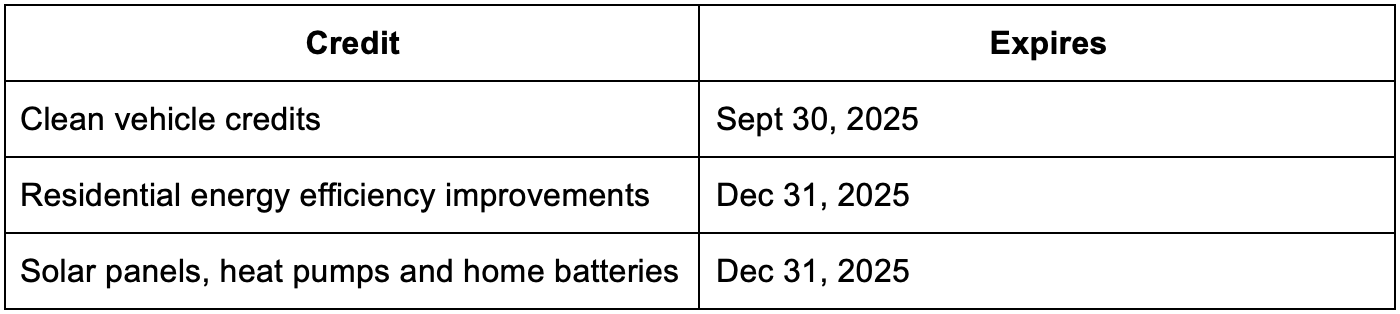

Energy credits are being phased out

One of the bigger reversals in OBBBA is the elimination of many energy tax credits:

So, if you’re planning to lean into green and buy an EV or install solar, 2025 is your last chance to benefit from these tax incentives.

Business provisions that matter

OBBBA includes several important changes for businesses:

● 100% Bonus Depreciation Returns

Purchase eligible assets after January 19, 2025 and claim 100% bonus depreciation. That means writing off the full cost of equipment in the year it’s placed in service. Qualified production property is a new class of assets also qualifying for 100% bonus depreciation.

Example: A contractor buys $150,000 of new machinery in February 2025. Under OBBA, they can deduct the full $150,000 on their 2025 return.

● §179 Expensing Limit Increased

Section 179 expensing also gets a boost for assets placed in service after December 31, 2024. While IRS inflation adjustments affect specific limits, the cap is now higher, offering businesses another way to write off major purchases.

● Immediate Deduction of Research Expenses

Businesses can now immediately deduct qualified research expenses, rather than amortizing them over time. There’s also an option to deduct previously amortized research costs, which may unlock further deductions.

● Interest Deduction Rules Relaxed

Business interest deduction rules under §163(j) are now more favorable, particularly for businesses with heavy capital needs. This change is technical, but for some taxpayers, it means they can claim more interest expense each year.

Final thoughts: what you do now matters later

Sure, the One Big Beautiful Bill Act has a lighthearted name, but its changes are serious. And in many cases, immediate.

If you own a business, manage real estate, or are planning large purchases or transfers of wealth, use this information to guide your tax strategy on how and when to act.

Now is the time to ask:

● Am I using the best structure for my business income?

● Should I accelerate planned purchases or energy improvements into 2025?

● How will these changes impact my property and estate planning strategy?

Knowing the answers to these questions could be the difference between a tax-savvy return and a missed opportunity.

If you’re not sure where you stand, talk to your tax advisor now, before the window of opportunity closes.

For a comprehensive look at how OBBB affects your real estate, click here.

Contact us to work on your tax strategy: info@ascendadvisors.com