While many Americans were celebrating the Fourth of July fireworks, the One Big Beautiful Bill Act (or OBBBA as some are calling it) made a bold entrance into the tax code, and it’s packed with updates that could impact how taxpayers plan, deduct and invest.

The OBBBA could have lasting effects for business owners, property holders and high-income earners. To help unpack it, we sat down with Ascend Tax Director Ron Hauser, a senior tax advisor with expertise in real estate and high-net-worth individuals, to break down key changes within the bill.

Here’s what you need to know, and how to act on it, before the opportunity window closes.

SALT deduction limit increased, but the PTE is still relevant

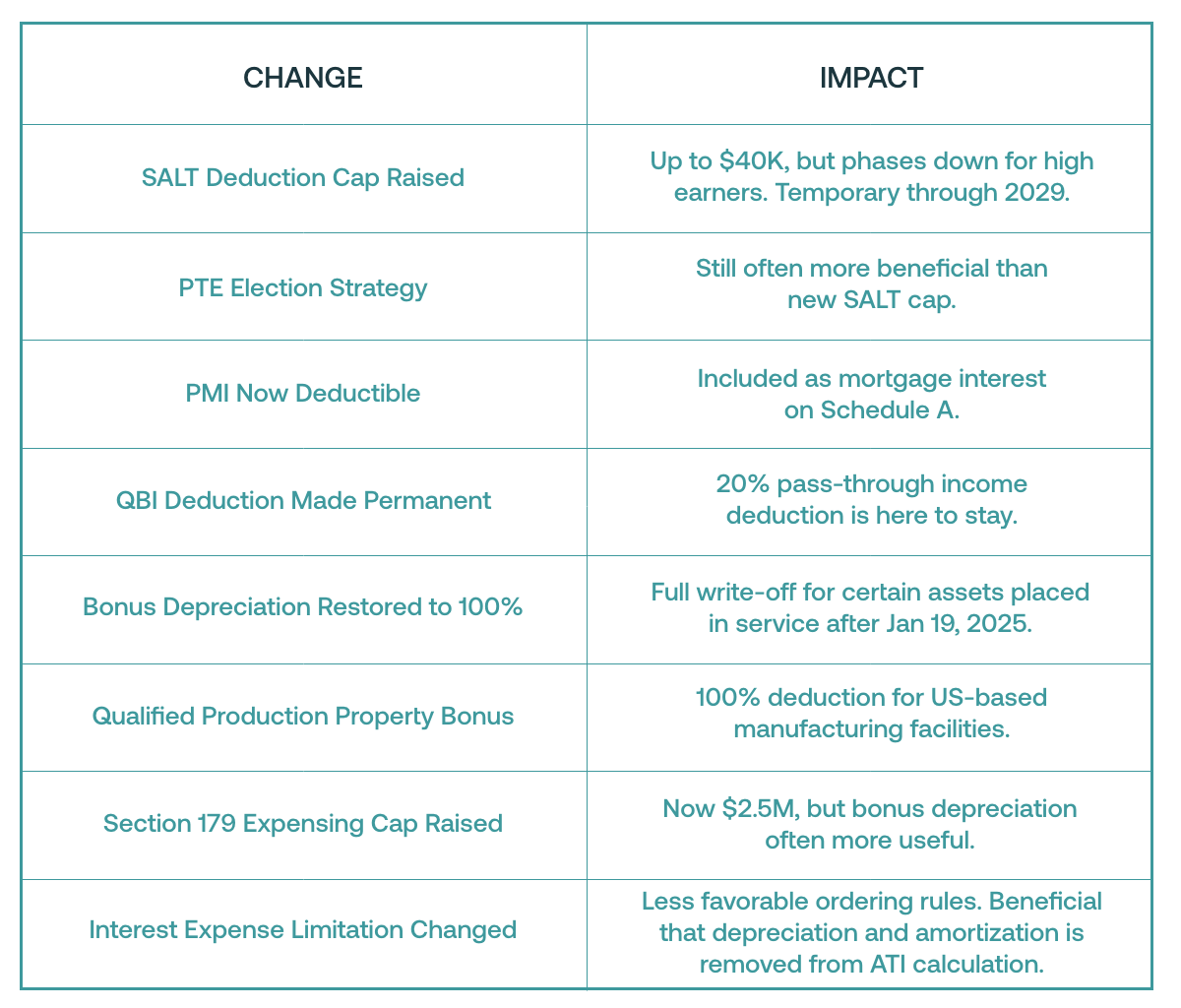

One of OBBBA’s more widely discussed changes is the increase to the personal SALT (state and local tax) deduction limit. Previously capped at $10,000, it has now been raised to $40,000.

“A $40,000 deduction is great, but it phases down to $10,000 for high-income earners,” says Ron. “And, it’s only through 2029, too,” he adds.

In other words, the expanded cap may be significantly reduced depending on your income level.

That’s why Ron still recommends using the Pass-Through Entity (PTE) tax election, where available. For many clients, it can offer a more consistent and generous deduction than relying on the new SALT limit rules.

“The PTE tax payments are still very relevant,” he says. “If you’re a partner in a partnership or a shareholder in an S Corp, and the election’s available to you, I encourage you to consider that option.”

Ron points out that this applies even to casual real estate arrangements, such as short-term rentals.

“Let’s say someone runs an Airbnb or owns some rental real estate with their spouse and they’ve just been reporting it on their personal tax return,” he explains. “It might be beneficial to start reporting that on a partnership return instead. You essentially now report on a partnership return what previously already existed on your personal return with your spouse,” he says. “And, you’re getting the added benefit of that state income tax deduction if you utilize the PTE election, where you otherwise may have been limited,” Ron says.

In short, the increased SALT deduction may sound like a win on paper, but Ron is clear: the PTE election remains one of the most strategic ways to maximize the benefit of paid state taxes.

Mortgage interest and PMI equal small gains for homeowners

Homeowners benefit from a modest but functional win: Premium Mortgage Insurance (PMI) is now deductible as mortgage interest.

“If you didn’t put 20% down and have to pay PMI, you can now write that off on Schedule A,” Ron says.

The mortgage interest deduction cap, tied to $750,000 in outstanding principal, remains unchanged. However, for new buyers, the added deductibility of PMI could prove a beneficial change.

QBI deduction is now permanent

First introduced in the 2017 Tax Cuts and Jobs Act, the 20% Qualified Business Income (QBI) deduction for pass-through businesses was set to expire, fueling speculation and uncertainty over whether the government would extend the deduction. OBBBA makes it permanent.

“It’s here for good,” Ron says. “Unless some other law passes to repeal it, there’s no expiration date.”

This stability gives business owners more confidence to strategize around. The deduction remains subject to income limits and business-type restrictions, but it’s no longer a temporary bonus.

Bonus depreciation returns to 100%

With OBBBA bringing back 100% bonus depreciation for qualified purchases made after January 19, 2025, businesses can once again deduct the full cost of qualifying assets in the year they’re placed in service.

Businesses can immediately deduct the full cost of equipment, furniture and other eligible assets, which means no smaller multi-year depreciation deductions.

“It’s a big deal,” Ron says. “Clients love this deduction.”

Importantly, bonus depreciation is optional.

“Just because it’s available doesn’t mean you should take it,” Ron adds. “If your business is already in a loss position, it might be smarter to defer and spread the deduction.”

Qualified Production Property is a new category worth knowing

A standout addition to OBBBA is the creation of ‘Qualified Production Property,’ which aims to bolster U.S.-based manufacturing. If you build or expand a facility to produce tangible goods, you can claim 100% bonus depreciation.

“Let’s say you build a $1 million factory. Under old rules, you’d deduct a little over $25,000 a year over 39 years,” Ron explains. “Now, you can deduct the entire $1 million in year one, provided you place it in service during the window.”

To qualify:

● Construction must begin after Jan 19, 2025 and before Jan 1, 2029;

● The facility must be placed in service from July 4, 2025 through Jan 1, 2031;

● It must be used for U.S.-based production of tangible goods.

● Original use commences with the taxpayer, for an integral part of qualified production activity.

“If you’ve been putting off a manufacturing expansion, now’s the time to get serious,” Ron says.

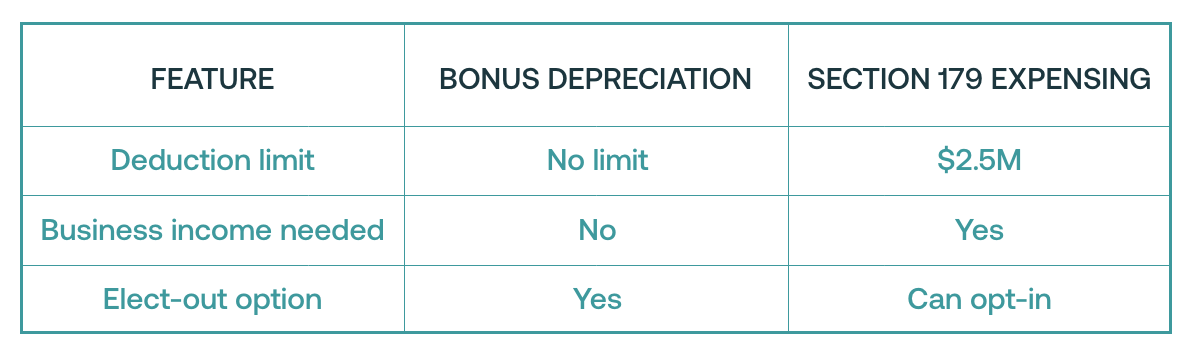

Section 179 is still here, but less dominant

OBBBA increased the Section 179 expensing limit to $2.5 million. While similar to bonus depreciation in allowing full write-offs, it has more rules and limits.

“There are still assets that qualify for 179, but not bonus,” Ron notes. “But for most clients, bonus depreciation is now the go-to. Section 179 is great for certain assets if you have the business income, but if you don’t, the deduction gets suspended.”

Interest expense limitation receives a big rule flip

One of the most technical and, according to Ron, potentially most problematic changes in OBBBA is how it modifies the treatment of business interest expense, particularly for leveraged real estate projects.

Previously, for businesses capitalizing interest and also subject to interest limitations, the IRS required you first to capitalize the interest related to construction or development. That capitalized amount became part of the building’s or construction project’s basis and could be depreciated over time. Whatever interest remained was then subject to the 30% limitation, based on your Adjusted Taxable Income (ATI).

OBBBA reverses that sequence.

“Starting after December 31, 2025, you now apply the 30% limitation first, and only capitalize what’s left,” Ron explains. “That means both your current deduction and your future depreciation could be reduced.”

However, the law also has a positive update regarding the calculation of ATI. Depreciation and amortization are no longer subtracted in arriving at ATI, which may increase the amount of interest a taxpayer can deduct.

“That part is beneficial,” Ron says. “But the ordering flip is not,” he adds, unapologetically unimpressed by this section of the new tax law.

The problem is cumulative. Under the old rules, taxpayers could at least recover disallowed interest later through depreciation. With the new order, that recovery is limited from the start.

“We need to be advising our clients about this,” Ron emphasizes. “If we’re not aware of it, it could be less beneficial than they expect.”

This change may not affect every taxpayer, but for developers and investors with high debt loads, it could quietly erode deductions in ways that aren’t immediately obvious.

THE ONE BIG BEAUTIFUL TAX BILL SUMMARY

Final thoughts are to plan early

Ron’s biggest advice? Consult with your CPA before making significant financial decisions.

“So many people tell us about their business decision after it’s already done,” he says. “I’m not saying CPAs should control your business decisions, but a quick conversation could save you.”

Whether it’s timing depreciation, forming a partnership, or rethinking how to structure an investment, the benefits of OBBBA will go to those who plan, not those who rush to file in April.

“Tax consulting is more than just meeting compliance deadlines,” Ron says. “Effective work and the real savings happen in the planning.”

Contact us to work on your tax strategy: info@ascendadvisors.com