Understanding how taxes work isn’t just for accountants or the ultra-wealthy; it’s for anyone who earns income and wants to hold onto more of it. But we get it: the U.S. tax code wasn’t built for simplicity. Many people go through the motions of filing and hoping for the best without realizing they could significantly reduce the amount they owe.

Ascend Director Jose Calles breaks down the overlooked and underused strategies that could reduce your tax bill. Whether you’re a salaried employee, savvy investor, or self-employed hustler, this guide gives you a clear path to keeping more of your money where it belongs: yes, with you.

Strategy #1: use your paycheck as a tax shield

Do you assume you don’t have tax options because you’re a W-2 employee? Think again. There are levers to pull that can significantly lower your tax bill if you know where to look.

- Bolster Your 401(k)-retirement plan

“Maximize your retirement contributions,” Jose advises. “Most employers offer 401(k) retirement plans.”

For 2025, the contribution limit is $23,500. If you’re 50 or older, an additional $7,500 catch-up raises the total to $31,000. This money is taken out pre-tax, which means it reduces your taxable income now.

Say you earn $120,000 and contribute $31,000 cap. Your taxable wages are based on $89,000, not the full $120,000.

“This is what we call a pre-tax deduction,” Jose explains. “You get the benefit right now.”

If your employer doesn’t offer a retirement plan, you still have options. “Consider an IRA account, where you can contribute $7,000,” Jose says. “If you’re over 50, that maximum increases to $8,000.”

To receive the same upfront tax benefit as a 401(k), this would need to be a traditional IRA, not a Roth. Roth IRAs offer different advantages, which we cover in a later section. These contributions, whether to a 401(k) or an IRA, are one of the most effective ways to reduce your current tax liability while saving for your future.

- Contribute to an HSA or FSA

A second overlooked paycheck strategy? Pre-tax medical accounts. “You can contribute money into a health plan and use it for medical expenses. Those are also pre-tax deductions,” Jose explains.

- Health Savings Account (HSA) limits for 2025: $4,330 individual / $8,550 family (+$1,000 catch-up if 55+)

- Flexible Spending Account (FSA) limit for 2025: $3,300

If your employer offers these plans, use them. These accounts let you pay for everyday health costs with untaxed dollars.

Strategy #2: play the long game with after-tax contributions

Pre-tax accounts lower your taxes now. But what about your future? After-tax contributions like Roth IRAs and Roth 401(k)s won’t give you an immediate deduction, but the payoff comes in retirement.

- Roth IRA and Roth 401(k)

“The benefit of a Roth is that all the appreciation over time is tax-free on retirement,” Jose says.

The 2025 limit for Roth IRAs is $7,000 (or $8,000 if you’re 50 or older). While you don’t save on taxes today, your withdrawals in retirement, including all growth, are completely tax-free. Handy for that Caribbean holiday you’ve been dreaming about.

This is ideal if you expect to be in a higher tax bracket later or if you just want future peace of mind. Be sure to check income limits to confirm your eligibility.

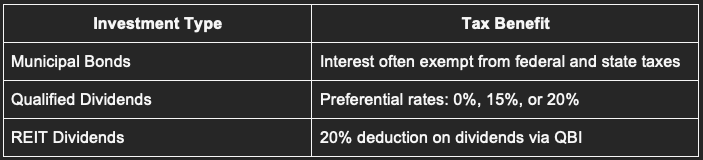

Strategy #3: Choose investments that give you an edge

Where you put your money is just as important as how much you save. Jose recommends focusing on assets that offer more favorable tax treatment.

- Municipal Bonds: Quietly Powerful

“Ideally, it would be good to have investments in municipal bonds from your home state,” says Jose. Why? Because they’re often exempt from both federal and state income taxes.

These low-key investments don’t shout, but they keep more of your return in your pocket.

- Qualified Dividends: Better Returns, Lower Rates

“If you’re considering some tax-efficient investments, consider securities that pay you qualified dividends,” says Jose. “Qualified dividends have more favorable tax rate treatment. If they meet IRS criteria, they may be taxed at 0%, 15%, or 20%, depending on your income.”

Seek out investments that pay qualified dividends instead of ordinary ones, especially if they offer similar returns.

- REITs: Real Estate with a Tax Twist

REIT (Real Estate Investment Trust) dividends are taxed at your ordinary rate. But they qualify for a 20% deduction through the Qualified Business Income (QBI) provision.

“For example, if you receive $10,000 in REIT dividends, you’ll only pay taxes on $8,000,” says Jose.

Strategy #4: capital gains, timing is everything

Taxes aren’t just about how much you earn. They’re about when you earn it. Selling an investment at the right time can significantly change what you owe.

- Hold for a Year (or More)

“Ensure you can hold the investment for more than 12 months,” Jose recommends. Long-term gains are taxed at lower rates (0%, 15%, or 20%) compared to short-term gains, which are taxed as ordinary income.

- Harvest Your Losses

“Consider tax-loss harvesting,” says Jose. “This involves selling losing investments to offset your gains.”

You can deduct capital losses up to the amount of your gains. If your losses exceed your gains, you can deduct up to $3,000 against your ordinary income and carry the rest forward.

Strategy #5: Itemize When It Makes Sense

Standard deductions are easy, but they’re not always your best move. Jose says, “If all of your itemized deductions are greater than your standard deductions, you get the benefit for it.”

Consider These Itemized Deductions:

- Mortgage interest

- State and Local Taxes (capped at $40,000)

- Charitable donations

- Medical/dental expenses over 7.5% of AGI

And if you're over 70½, consider a Qualified Charitable Distribution (QCD) from your IRA. It doesn’t count as taxable income and can help fulfill your Required Minimum Distribution.

Strategy #6: self-employed? Lean into the tax code

If you run your own business, you get access to a much broader toolkit. But many sole proprietors don’t know what they’re entitled to.

- Deduct Necessary Expenses for Business Operation

“Sole proprietors can deduct all the ordinary necessary business expenses,” Jose says. This may include office supplies, software, internet, and advertising.

- Health and Retirement Are Deductible

You can deduct 100% of your health insurance premiums for yourself and your family. You can also deduct half of your self-employment tax.

Set up a SEP-IRA or similar plan to maximize retirement deductions based on your business income.

- Use the Home Office and Vehicle Deduction

If you work from home, the portion of your home used exclusively for business is deductible. Business mileage in 2025 is worth 70 cents per mile, or you can also use actual vehicle expenses, whichever is more beneficial.

Strategy #7: beat the IRS to the punch with estimated payments

Tax planning isn’t just about deductions; it’s also about timing. If you don’t pay your taxes throughout the year, you could face underpayment penalties.

- The Safe Harbor Rules

To avoid penalties:

- Pay 90% of your current year’s expected tax

- Or pay 110% of your prior year’s tax (100% if your income is under $75K single / $160K joint)

Estimated payments are due:

- April 15

- June 15

- September 15

- January 15 (of the following year)

“If you’re underpaid, the penalties and interest at the end of the year could be significant,” Jose warns. For high-income clients, he recommends quarterly planning.

The tax mistake that can cost

According to Jose, the biggest error is acting before asking.

“Make sure, before making any big decisions or transactions, always consult your tax advisor,” Jose reminds us. “So that we can plan accordingly.”

“Not discussing things like the sale of a house or investment before talking to us can be detrimental,” Jose says. “At that point, without that upfront discussion, it limits our ability to strategize.”

Every major financial decision has a tax consequence. Don’t wait to find out the hard way.

Final thoughts

The best time to plan your taxes isn’t April; it’s year-round. Smart tax strategy isn’t just for high-net-worth individuals. It’s for anyone who wants to keep more of what they earn.

Whether you’re salaried, self-employed, or somewhere in between, the tools are there. Retirement accounts, smart investments, strategic deductions, and proactive planning can all reduce your liability if you know how to utilize them effectively.

Take the time. Learn the strategies. Then, file with confidence.

Want to strategize to your individual needs? Contact us at info@ascendadvisors.com.